While most undergrads were out drinking whatever they drank in the 30s, Ronald Coase was working on a theory that would help him win the Nobel Prize 50 years later.

In “The Nature of the Firm”, Coase demonstrated why businesses must exist at all, instead of individuals just contracting directly with each other. At the core of his rationale was transaction costs: costs incurred on top of the actual price paid for a good or service due to the need to coordinate and execute the transaction itself. Businesses reduce these costs, for example by hiring a full time employee instead of having to sign a new contract for every project they complete.

Carl Dahlman later gave us the three categories that are widely used today:

- Search and information costs: discovering what is available to purchase and comparing alternatives

- Bargaining and decision costs: coming to an agreement between buyer and seller, including establishing the final price and terms

- Enforcement and policing costs: ensuring that both sides holds up their end of the deal

While not formally included, there is another major cost that is commonly incurred on top of the price of the good or service itself:

- Distribution costs: actually getting the good or service to the end consumer

Marketplaces are simply businesses that don’t sell goods or services, but instead sell the reduction of transaction costs. As a result, studying transaction costs will help you understand where marketplaces will succeed, what kind of marketplace to build, and how to price them.

Transaction costs explain which industries to target and how much potential there is to expand TAM

Bill Gurley wrote the canonical piece on the conditions that make an industry a good fit for a marketplace. If you study the list, you’ll realize that most of the conditions indicate either (1) the presence of high transaction costs, (e.g. high fragmentation) or (2) the ability to reduce those costs (e.g. creating economic advantages vs. status quo). These are the two most important factors to predict the potential for a successful marketplace.

Here are examples of industries that suffered from each form of transaction cost, and how a marketplace fixed it:

Search and information costs: Extreme fragmentation of suppliers in the handmade goods industry previously made it very hard for buyers and sellers to find each other. Etsy solved this by giving sellers tools to list everything on their marketplace, and giving buyers easy search and filtering.

Bargaining and decision costs: Price transparency used to be a key problem when hiring a taxi. Your only option was to get in the car and watch the meter run up. Now Uber calculates the price ahead of time, making it easier to decide whether or not to take a ride.

Enforcement and policing cost: Independent retailers have a hard job. One reason for this is inventory risk: if they buy something that doesn’t sell, they previously had to just eat the cost of goods. To cope, historically most new wholesale relationships were formed live at trade shows so retailers could vet the product in person. This works relatively well, but is also exceptionally costly and time intensive. Faire solved this by pairing online checkout to net payment terms and free returns to de-risk the transaction.

Distribution costs: Having a dedicated delivery fleet is prohibitively expensive for most independent restaurants, forcing customers to spend the time to pick it up themselves or go without. Postmates and Doordash solved this by building fleets that restaurants can effectively rent.

As marketplaces reduce transaction costs, the effective cost of a good or service goes down, increasing demand and growing the market. The degree of TAM expansion is closely related to the percentage of total cost that is eliminated. [1]

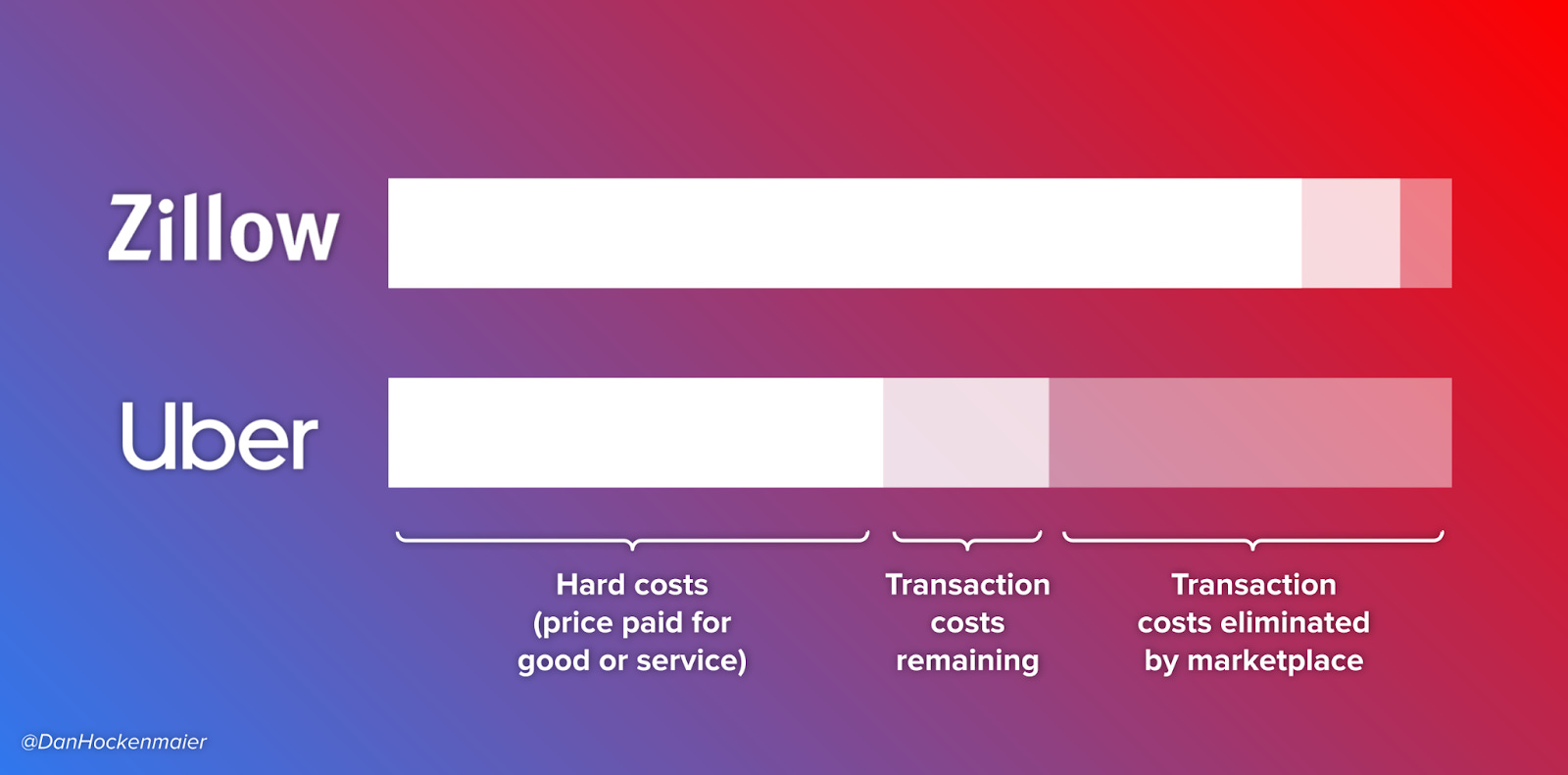

Let’s look at two extremes: buying a home and hiring a taxi.

It's a lot of work to search for homes, and Zillow makes that easier. But that cost is a small fraction of the largest purchase most people will ever make, and they still have to tour, negotiate, close, and actually move in. Zillow lowers the effective total cost of buying a home, but not by much. As a result, the TAM expanded very little.

In contrast, before Uber the transaction costs associated with hiring a taxi were often more than the cost of the ride itself. You might pay $15 for the ride, but before that you had to call a cab company, wait 45 minutes for a car that might never show up, and only find out the price once you arrived.

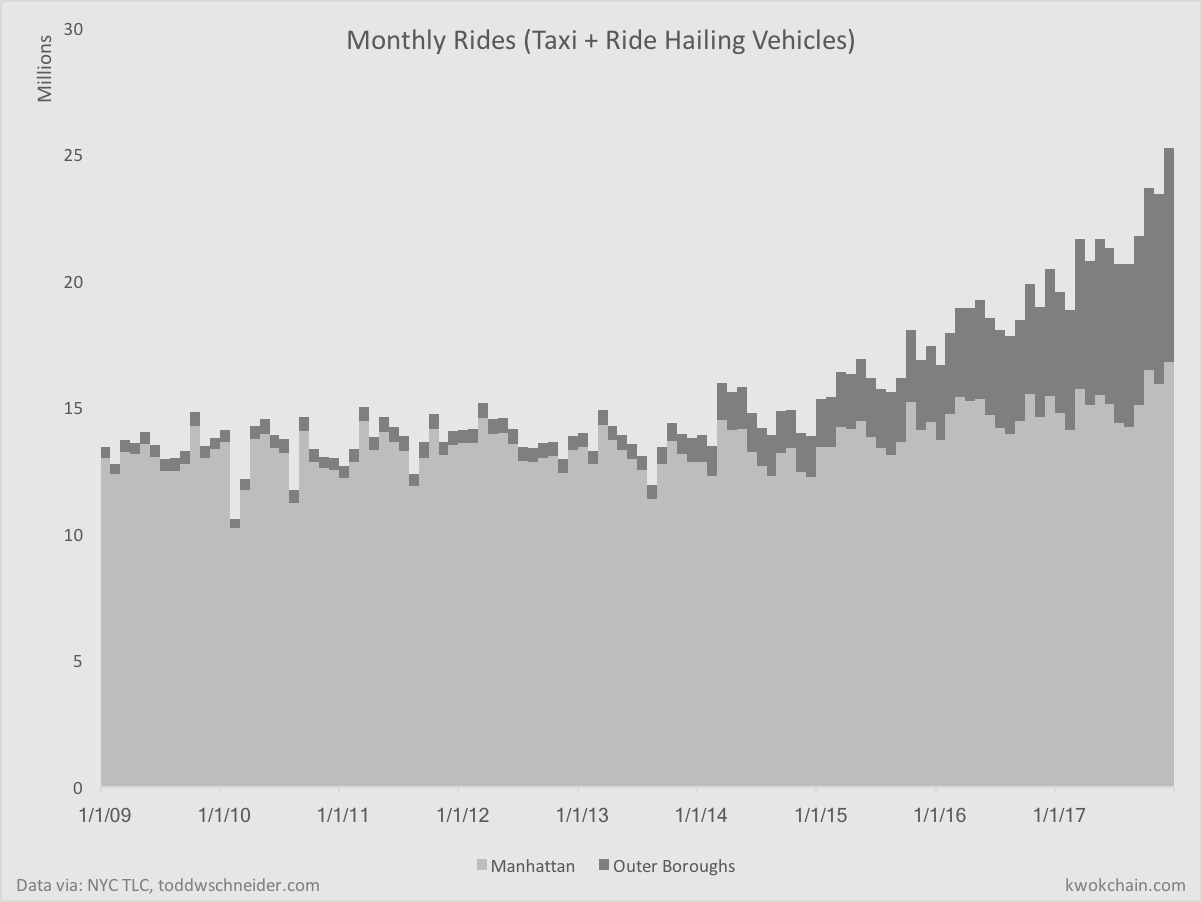

Kevin Kwok wrote a great piece about how Uber and Lyft grew the TAM for private cars. Not only that, but they grew TAM precisely in areas where transaction costs were highest. In New York, demand jumped in the outer boroughs, with much more modest gains in Manhattan where hailing a yellow cab was already relatively easy.

Transaction costs explain how marketplaces have evolved, and where there are disruption opportunities

When marketplaces enter an industry for the first time, they win because they remove transaction cost relative to analog options. When a marketplace disrupts an older one, they win because they remove more transaction cost than their predecessors.

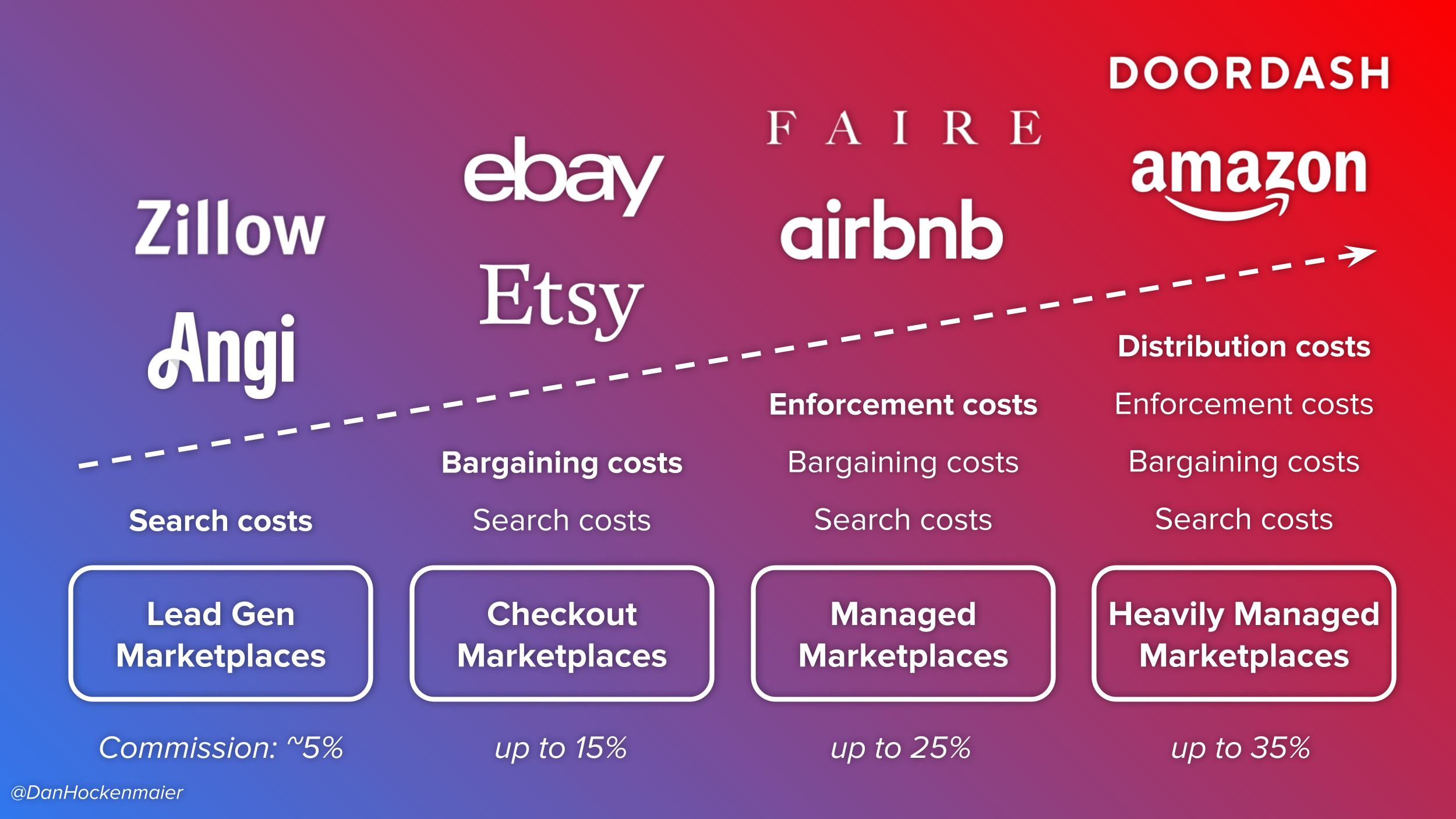

The 4 buckets of transaction cost are a good way to define the four stages of marketplaces. (The inspiration for these categories comes from this piece by Casey Winters and Gilad Horev).

Lead generation marketplaces like Zillow and Angi address search and information costs, but stop there. They build an index of what is available and make introductions between buyers and sellers who are then mostly on their own to negotiate and carry out a transaction.

Checkout marketplaces like Ebay and Etsy also address bargaining and decision costs, by setting prices and terms upfront and allowing for real-time checkout. Because they have more data on which transactions are happening and with which sellers, they typically also have a much more robust ratings and reviews system to reduce the decision cost of choosing a seller.

Managed marketplaces like Faire and Airbnb solve for enforcement costs, by bearing the financial risk of something going wrong through guarantees, return policies, and payment terms. This is distinct from simply providing information to help buyers make good decisions: to be a managed marketplace, you must directly bear the financial risk.

Heavily-managed marketplaces like Doordash and Amazon take it one step farther and actually participate in the distribution of goods or services on behalf of their sellers.

Most industries don’t stay in one stage for long. Amazon evolved so aggressively that they didn’t make room for anyone else to cut in, starting with a checkout marketplace but then quickly layering in free returns to solve for enforcement costs and FBA to solve for distribution.

Many other marketplaces lost ground as their industry evolved. Ebay lost share in the sneakers category because GOAT and StockX jumped from checkout to managed marketplaces by taking on verification and guarantees directly. And Grubhub lost market leadership altogether because the next generation of food delivery marketplaces including Postmates and Doordash launched as heavily managed marketplaces with built-in distribution.

Transaction costs explain how to monetize a marketplace

The amount a marketplace can charge is driven by how much of the transaction cost they can remove. As we see in the graphic above, there is an increase in potential commission for each stage of marketplace: they are doing more work for sellers and buyers sellers, and charging more for it.

If a marketplace creates enough value and distributes that value effectively, everyone wins, and especially buyers. When all is said and done:

- The buyer’s effective cost is much lower. They enjoy an easier experience to find, buy, and guarantee purchases, and don’t have to pay extra for it.

- The seller’s effective cost is similar before and after a marketplace arrives. They have lower transaction costs, and pay the marketplace for this value. They do however have a more scalable customer acquisition channel, and there are more customers to go around, so their businesses grow.

- The marketplace is able to keep a fraction of the value they create in the form of gross margin, because they solve the seller’s problem more efficiently than sellers were doing it themselves.

It plays out like this because long term virtually every marketplace is demand constrained. If you can give a seller more customers, as long as they are at least as profitable as their existing business, they will usually take them. So marketplaces are incentivized to charge as much as they can of sellers (which ends up being about what they were paying before), and compete by giving as much value as they can back to buyers to aggregate demand and grow the market.

To understand how this happens in more detail, let’s look at two groups of transaction costs that behave very differently as the economic value is shifted around:

Transaction costs with low variable costs: Search and Bargaining costs

Solving for these costs is as close as you can get to a “free lunch”. It is simply much more efficient to search for and buy things online, and it doesn’t cost much to enable this at scale. This was the magic of the early marketplace business models like Ebay.

In doing this, marketplaces save sellers a lot of money, because they no longer need to spend time or hire more people to search for and negotiate with customers. Marketplaces typically charge sellers about what they were paying to do this themselves, and keep the efficiency they’ve created.

Marketplaces also make the buyer’s lives much easier: it is now much faster and easier to make a purchase. Typically marketplaces let buyers keep that value vs. charging for it, because if they do charge it makes them vulnerable. Angie’s List had a tidy business charging customers a subscription fee for the convenience they created, until HomeAdvisor and Thumbtack ate their lunch by giving it away for free, opting to only monetize on the supply side.

Transaction costs with high variable costs: Enforcement and Distribution costs

In contrast, there are high variable costs associated with taking on enforcement costs (e.g. funding free returns) and distribution (e.g. building a logistics network).

As marketplaces move into the managed and heavily managed stage and take on these costs, they usually become bigger businesses, but if anything their margins get worse. This is a tell for what is happening underneath the hood: they are making enforcement and distribution more efficient, but then giving all of that value back to buyers to compete with other marketplaces, and in doing so further growing the market.

For example, Amazon uses Prime as a customer acquisition and retention tool, not a monetization tool. And Doordash mostly charges customers what it actually costs them to provide delivery, or even less if you are using DashPass, a trade they are willing to make because it improves retention.

The silver lining is that winning at enforcement and distribution tends to be more defensible precisely because it is harder. it takes a lot of scale and highly efficient operations and underwriting to win, which is difficult to replicate.

Implications

The concept of transaction costs gives us a lot of explanatory power in predicting what will come next for marketplaces. A few high level observations:

In most industries, the “free lunch” value creation opportunities are exhausted. Marketplaces must increasingly push into activities with high marginal costs. They are likely to become higher scale but also lower margin and increasingly operationally and analytically intensive to run. As part of this evolution, we will see marketplaces go beyond the costs we’ve talked about here altogether, and start to take on the cost of the good or service themselves, for example by manufacturing on behalf of sellers. This will result in some industries ultimately vertically integrating and graduating out of marketplace models altogether. As I wrote about here, businesses that need the creativity of their sellers to make buyers happy (think Etsy, Steam) are more likely to stay in marketplace mode long term.

To disrupt incumbent marketplaces, look for places that transaction costs remain AND which you can make much more efficient than the current solution. It was possible for Doordash to disrupt Grubhub by taking on food delivery because they could build a delivery network that is more efficient than a restaurant’s own sub-scale operations. But the same is not true if you wanted to disrupt Etsy, because there you would be competing with UPS and Fedex, who are very good at what they do. It would take Amazon scale and a massive investment to actually create a faster and cheaper shipping experience for customers.

By far the largest unsolved transaction costs remain in the services industries, like freelancing and home improvement. Services are two thirds of consumer spending. Yet while there are about 10 public marketplaces in the US with market caps over $10B, zero of them are in the services industries. Almost every services marketplace is stuck at the Lead Gen phase, massively limiting penetration and take rate. My next essay will be about why that is and what might finally open the floodgates.

--

Credits

Thank you to Casey Winters, Chris Erickson, and Forrest Funnell for their feedback on this essay.

--

Notes

[1] There are two other ways in which marketplaces expand TAM outside of transaction costs, neither of which contributes as much as transaction costs.

The first is reducing the actual prices that customers pay. Certainly we see this in the early stages of many successful marketplaces: for example both Airbnb and Uber broke out because they were cheaper alternatives to hotels and taxis respectively. However that reduction is largely driven by (1) bringing new supply online that was previously underutilized such as private bedrooms and cars and (2) marketplaces initially using VC to subsidize prices to grow share. Both of these have a tendency to normalize as markets mature and they are subjected to the same competitive dynamics that set the prices in the old regime. The price gap between Airbnb and Uber and legacy alternatives has mostly closed today.

The second is the new supply itself. If you can now choose between all of the hotels in Paris AND all of the open bedrooms in Paris, might you actually travel there more frequently? A 2014 study on Airbnb did find that about half of nights booked were incremental to hotels. But this was while Airbnb was still sub-scale, and it appears to be becoming less incremental over time. Most people have a set amount of budget and time they devote to vacations, so unless you can actually reduce the money or time costs of taking a trip, you’re unlikely to change demand meaningfully.